Pensioen Plus

- You supplement your retirement pension and surviving dependant's pension with a net pension

- You benefit from tax advantages

- You can adjust or terminate your choices each month

Supplementing your pension in the case of a higher salary

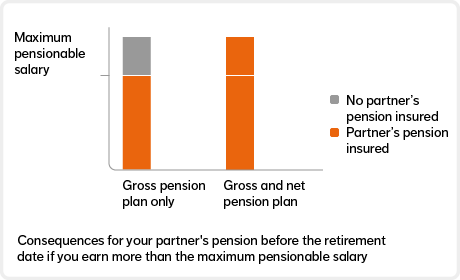

If you have a pension scheme through your employer, the Tax and Customs Administration imposes limits on the salary on which you accrue pension in this scheme. Above this maximum pensionable salary, you do not accrue pension and no partner’s pension is insured. The higher your salary, the greater the drop in your income when you retire. And the more your partner will have to give up in the case of your death. With Pensioen Plus you top up your pension again: with a net pension.

Would you like to receive a proposal for Pensioen Plus?

Does your employer offer you the possibility to participate in Pensioen Plus? Using the information your employer communicates to us, we assess whether you can participate. You will then receive a personal proposal from us automatically. Always discuss the proposal with a financial advisor. This way you will know whether Pensioen Plus is appropriate for your financial situation.

If you received a personal proposal before but did not accept it and you wish to participate now, complete the application and change form. You will find this form under the tab ‘Adjust’.

Financial advisor

If you do not yet have a financial advisor, you can find an independent financial advisor in your area. You pay this advisor yourself. Make proper arrangements about this in advance with the advisor.

Pensioen Plus is a supplementary net pension scheme for employees with a salary above the maximum pensionable salary (€137,800 in 2026).

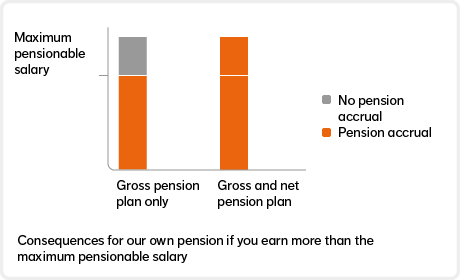

If your salary is higher, you will not accrue pension on your salary above this amount through the regular (gross) pension scheme of your employer. The higher your salary, the greater the drop in income when you retire. And the more your surviving dependants will have to give up in the case of your death. This is due to the limit set by tax rules on pensionable salary. The government does, however, make it possible to accrue a pension on the salary above the threshold: with a net solution. For this we offer Pensioen Plus.

The images show the consequences for your partner’s pension and retirement pension if your salary exceeds the threshold.

Consequences for your partner’s pension

Consequences for your retirement pension

Pensioen Plus is a defined contribution (DC) scheme. With Pensioen Plus you can:

- insure a supplementary partner’s pension in the period before the retirement date (package 1) and/or;

- supplement your retirement and partner’s pension in the period after the retirement date (package 2).

You pay Pensioen Plus from your net salary. On the other hand, you do not have to pay tax in box 3 (investment yield tax) on the amount that you accrue. You or your partner will also not pay tax on the lifelong benefit.

You can only use Pensioen Plus if your employer offers this possibility. It may be that your employer offers only Pensioen Plus package 1 or package 2. In that case, you can only use that part of Pensioen Plus. Check your Pension 1-2-3 in mijn.nn to find out what is possible for you.

How does Pensioen Plus work?

If your employer offers you Pensioen Plus, you have the possibility to supplement your pension over your salary above €137,800 (2026). You decide whether you want to. You can choose from the following options:

- Package 1: limits the loss of income for your partner and any children in the event of your death during employment.

- Package 2: supplements the retirement pension and partner’s pension from your retirement date.

- Combination of packages 1 and 2.

You can activate or deactivate these packages every month or change the amount you pay (your premium). Read more about the packages under 'package 1' and 'package 2'.

With package 1, you supplement the partner’s pension before your retirement date. You take out risk insurance for this purpose. If you die while you are still employed, your partner will receive a lifelong net benefit. If you die when you are no longer employed or when your pension starts, your partner will not receive any benefit from package 1.

With package 1, you also supplement the orphan’s pension.

Automatic insurance

If your employer offers Pensioen Plus, you will automatically be insured for this package from the time you earn more than the threshold amount. If you do not want this, you can waive this option. You can do so using the form that you receive with your proposal for Pensioen Plus.

Supplementation of partner's pension

Every year, as in your normal pension scheme, we calculate the monthly amount your partner will receive in the event of your death. The amount of this lifelong net benefit depends on your salary above the maximum pensionable salary. However, an upper limit of € 1,000,000 applies by default. Your partner's benefit may increase annually by the same percentage as in your normal pension scheme.

Supplementation of orphan’s pension

Supplementation of orphan’s pension is automatically co-insured. If you die before your retirement date, your children will receive a supplementary net orphan's pension up to a certain age. You cannot choose separately to supplement the orphan’s pension.

Tax benefit

Your partner and possibly your child or children do not have to pay wage tax and inheritance tax on the net pension benefit. The benefit falls under the exemption from inheritance tax. The exemption for the remainder of the inheritance is, however, reduced as a result.

If you become occupationally disabled

If you become wholly or partially occupationally disabled, Nationale-Nederlanden will continue to pay all or part of the premium for Pensioen Plus for you. We do this for as long as you are wholly or partially occupationally disabled. This premium increases with age and is determined annually.

No medical examination in the case of participation within four months

If you participate within four months, you will not have to fill in a medical questionnaire or undergo an examination. The four-month period starts from the time that you can participate in package 1. This is the case, for example, if your salary rises above the maximum pensionable salary, you commence employment or enter into a partnership.

If you want to participate at other times, or if you want to change your choices, we may ask questions about your health and have you undergo an examination if necessary.

With package 2, you supplement your retirement pension and partner’s pension after the retirement date. You do so by accruing an amount with investments. On your retirement date, you buy a net retirement pension and a net partner's pension using this value of the investments.

Tax benefit

You do not have to pay investment levy (box 3) on the value of your investments. You or your partner do not have to pay wage tax on the benefit. Neither does your partner have to pay inheritance tax on the value of the benefit. This is because the benefit falls under the exemption from inheritance tax. The exemption for the remainder of the inheritance is, however, reduced as a result.

Flexible contribution

You pay a monthly premium from your net salary via your employer. The table shows the maximum percentage of your salary above the salary threshold (€137,800 in 2026) that you can contribute. From this amount, you decide what percentage you contribute: 50%, 60%, 70%, 80%, 90% or 100%. You can increase, decrease or stop paying your premium (paid-up premium) every month.

How much can you deposit?

| Age | Percentage |

|---|---|

| 15 to 19 | 3,43 % |

| 20 to 24 | 3,91 % |

| 25 to 29 | 4,51% |

| 30 to 34 | 5,19% |

| 35 to 39 | 5,92 % |

| 40 to 44 | 6,83 % |

| 45 to 49 | 7,90 % |

| 50 to 54 | 9,10 % |

| 55 to 59 | 10,52 % |

| 60 to 64 | 12,06 % |

| 65 to 67 | 13,39 % |

Additional choice: benefit in the case of death before the retirement date

If you opt only for package 2, you have an additional choice.

With the value of the investments, you purchase your retirement pension and partner’s pension after the retirement date. If you die before your retirement date, this value is cancelled. Would you like to receive a benefit for your surviving dependants if you die before your retirement date? If so, you can select this option on the application form. Upon your death, your surviving dependants will receive a benefit of 90% of the value of the investments. They use this to buy a net partner’s pension and possibly a net orphan’s pension.

If you become occupationally disabled

If you become wholly or partially occupationally disabled, Nationale-Nederlanden will continue to pay all or part of the premium for Pensioen Plus for you. We do this for as long as you are wholly or partially occupationally disabled. This premium increases as you get older.

If your employer offers Pensioen Plus, and your salary is higher than the maximum pensionable salary, you will receive a letter from us with personal calculation examples. It also shows the total costs and premiums. You can activate or deactivate packages yourself, and you can choose a different premium percentage for package 2. This way you can always tailor your Pensioen Plus to your personal situation.

Overview of costs and risk-based insurance premiums

Below is an overview of the costs and risk-based insurance premiums for Pensioen Plus:

- Risk premium for package 1: you pay this for the insurance that pays out the net partner's pension and net orphan's pension if you die during your employment. Your letter with personal calculation examples shows how much risk-based insurance premium you pay.

- Premium for package 2: you pay this for the accrual of an amount with which you supplement your retirement pension and partner's pension after the retirement date. You buy this pension with the value of the investments on your retirement date. Your letter with personal calculation examples shows how much premium you pay.

- Investment costs for package 2: if you invest in lifecycles, you will pay an annual investment fee of 0.40% - 0.45% (ongoing charges plus management fees). The exact investment costs depend on your investment choices and age. For the current investment costs go to nn.nl/fondsen-ivab (in Dutch), click on the fund name and open the PDF to view the costs. Remember: some investment funds charge a performance fee.

- Risk-based insurance premium for contribution waiver in the event of occupational disability: for continued payment of contribution at Nationale-Nederlanden if you become occupationally disabled.

- For Pensioen Plus, you pay no administration costs.

Do you want to participate in Pensioen Plus at a later date? Or do you wish to adjust or cancel your Pensioen Plus?

- I wish to participate in package 1 and/or 2

- I wish to adjust package 2

- I wish to cancel packages 1 and/or 2

For this purpose, use the change form.

Do you wish to adjust your investment choices for Pensioen Plus?

- I wish to adjust my investment choices for lifecycle investment. Go to the ‘Adjust’ tab and scroll through to Adjust investments for your Pensioen Plus.

- I want to switch to Self-investment or adjust my investment choices for Self-investment. Go to the Self-investment tab and scroll through to Adjust investments for your Pensioen Plus.

Service and Contact

We can help you in various ways.

Do you have a question?

You can handle many requests by yourself. Or you can contact us.

Would you like advice?

Together with an independent advisor, you look at which product suits you.